When it came to mobile video and 3G, it was always a clear case of video killed the radio star, with the surge in demand for video delivered to smart devices completely overtaking the ability of networks and operators to manage. Based on my attendance at the Global Mobile Video Summit in Berlin, it seems that things are changing.

People are changing faster than technology

Mobile video has moved from niche interest to regular communications. Indeed Gail Smith of Cavell Group went further and stated that “the dominant medium for communications is becoming video”. Even if we don’t quite agree, it’s not hard to see shifts in people’s behaviour. Ten years ago, the industry disappointment we used to call “video calling” is now all the rage – but they call it Facetime or Skype Video, and is driven in part by those front-facing cameras on our smartphones and tablets. Furthermore, mobile video is increasingly being uploaded (not just downloaded) especially at sporting events and holiday destinations as a new “wish you were here” video trend becomes increasingly familiar. And of course, social networking is also propelling mobile video usage – it’s just so easy to click on that link in the Tweet you just received.

These trends are even causing macro level changes in the business of those working in “movies”. At the conference, John Nolan from North-One TV, lamenting the TV industry’s inability to monetise mobile, said “In the good old days, to make a movie you had to be rich, clever, and connected. Today, everyone is a producer and everyone is a distributor!”

Bigger screens, front-facing cameras, longer, richer videos, and the fact that people no longer need a PhD in Gadgets to work the camera on a phone – all of these are factors causing shifts in the way people are interacting and collaborating through video.

But technology is changing too

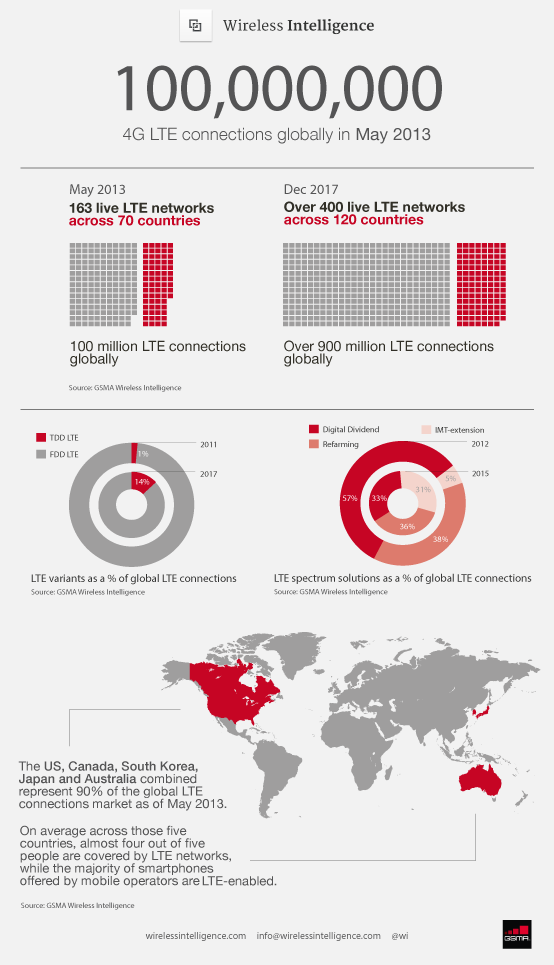

4G/LTE is called “LTE” for a reason, it’s a long-term evolution. Wireless Intelligence stated recently that there are now 100 million 4G/LTE connections. Wow! That’s a big number, right? Surprisingly, it’s a relatively small number when you consider there are around 3.4 billion unique connected users in the world. If you spin this statistic around, at least 97 percent of people in the world are not using LTE. As well as coverage there remain serious issues of interoperability between handsets which will persist for a long time.

But of course there are significant developments in LTE that do help advance mobile video consumption. First there’s the obvious: lower latency, higher throughput and spectral flexibility to aggregate carriers together. There is also the prospect of guaranteed QoS provided by more bandwidth, although that remains to be proven. Best of all, there is the new technology (not yet commercially available) of LTE Broadcast. For mass consumption, this point-to-multipoint broadcast of video content in a limited space (eg a sporting event), or in a limited time (eg breaking news), provides a colossal step-up in efficiency. It delivers rich video content to hundreds of users but using the bandwidth of only a single user. LTE Broadcast could certainly lead to new business models in the way mobile video is priced and distributed. In the end though, leaving aside disruptive technologies, we are still talking about limited radio spectrum which subscribers have to compete for. LTE is a helpful stop along the way but it is not our destination.

3G to 4G – lessons to learn

Three points.

First, the argument that “size matters” has been proven false (again). Mobile video optimization does reduce the volume of data in the network but that does not lead to automatic savings. More often, it leads to more users downloading more video, more of the time – and still causing congestion. Video optimization makes complete sense whenever and wherever congestion occurs, but not otherwise. Solutions such as congestion-triggered optimization are the key to achieving optimum use of bandwidth, not just minimum use of bandwidth. It’s a three-way balancing act between cost of optimizing, loss in QoE, and bandwidth savings. A more complex formula than “size matters”.

Secondly, more of a prediction than a lesson, ‘net neutrality in mobile is not going to fly. A few countries such as Chile and, as of last year, the Netherlands, have adopted stringent ‘net neutrality legislation for mobile, and the EU is currently wrapped up in discussions to bring about some measure of Europe-wide legislation. Rigid ‘net neutrality can only hold back deployment and adoption of mobile services. It’s one thing on fixed broadband to say that Internet Explorer should not be the only browser, and that traffic in big pipes should all be treated the same, but mobile networks are different. Mobile networks are inherently non-neutral. How can we say mobile networks are impartial when one side (operators) bears the burden of paying while another side (OTT players) takes the revenue? This inherent bias that has been built into mobile from day one cannot be defused by adding a veneer of “’net neutrality”.

Lastly, to state the obvious, monetization really matters. The low price per GB of video is causing margin erosion worldwide and contributing to declining revenues for European operators year-on-year.

Informa said recently: “Video streaming will account for a third of mobile data traffic on handsets in 2016; but money paid by mobile users for streaming will only amount to 0.6% of mobile data revenue”. This game has to change. And it is the right time to change. Today with the right technology in place, operators have the ability to treat every video flow individually, to decide in real-time how to charge for it, and how to achieve the best QoE. As we have stated before, some mobile operators, most notably US regional carrier C Spire have started to experiment with “video-as-a-service” and are offering packages such as two hour and five-hour video streaming plans, as well as tethering passes as add-ons to existing, low-cost plans. Although they have not made any figures public, this approach has directly contributed to increases in ARPU. Unsurprisingly, it seems that people will pay for what they want – as long as they understand what they are getting.

So changes in culture, yes; changes in technology, definitely; changes in revenue – just beginning.

__________

*Chris Goswami, PhD, Director of Marketing, Openwave Mobility has worked for 25 years in the telecoms industry. Within Openwave Mobility, Chris heads up Product Marketing, providing tactical support and business cases for areas of strategic interest. In his previous role in Openwave’s Global Solutions Team, he was responsible for coordinating solutions for complex customer problems in the mobile-data space.

*Chris Goswami, PhD, Director of Marketing, Openwave Mobility has worked for 25 years in the telecoms industry. Within Openwave Mobility, Chris heads up Product Marketing, providing tactical support and business cases for areas of strategic interest. In his previous role in Openwave’s Global Solutions Team, he was responsible for coordinating solutions for complex customer problems in the mobile-data space.

{kind=link}

This comment has been removed by a blog administrator.

ReplyDeleteThree stars on one screen, Pulkit Samrat, Yami Gautam, Urvashi Rautela in Bollywood movie sanam Re, check out the songs here.

ReplyDelete